What is the North America Green Tea Market Overview – definition, scope, and significance?

The North America Green Tea Market comprises the production, distribution, and consumption of green tea products across the United States, Canada, and Mexico. It includes a wide array of formats such as tea bags, instant mixes, iced beverages, and loose‑leaf teas, as well as flavored variants like lemon, aloe vera, cinnamon, vanilla, and basil. The market’s scope extends to retail channels ranging from supermarkets and hypermarkets to convenience stores and online platforms. Green tea’s health‑centric positioning—highlighting antioxidants, metabolism support, and low‑calorie attributes—makes it a significant driver of consumer choice in a region increasingly focused on wellness, functional beverages, and natural ingredients.

What are the North America Green Tea Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising health consciousness, demand for natural and low‑sugar beverages, and the expanding flavored‑tea segment that caters to adventurous palates. Convenience and accessibility through online channels further accelerate growth. Restraints stem from price sensitivity compared with traditional black tea and coffee, as well as supply chain complexities for high‑quality leaf sourcing. Challenges involve maintaining product consistency amid diverse processing methods and navigating regulatory scrutiny around health claims. Opportunities arise from product innovation—such as ready‑to‑drink iced green teas and functional blends with added botanicals—and from expanding distribution in specialty stores and e‑commerce platforms targeting younger, health‑oriented demographics.

What are the North America Green Tea Market Growth Trends?

Recent trends show a shift toward ready‑to‑drink (RTD) iced green tea, driven by on‑the‑go consumption patterns. Flavored green teas, particularly lemon and aloe vera, are gaining traction as consumers seek novel taste experiences. The premium loose‑leaf segment is experiencing modest growth among tea enthusiasts who value traditional brewing rituals. Additionally, the use of sustainable packaging and clean‑label formulations is becoming a differentiator for brands aiming to capture environmentally conscious shoppers.

How has COVID‑19 impacted the North America Green Tea Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains and halted in‑store sales, prompting a temporary dip in volume. However, heightened health awareness during lockdown periods spurred an increase in home consumption of green tea, especially bulk loose‑leaf and tea bags purchased online. Post‑pandemic, the market has rebounded strongly, with e‑commerce maintaining a larger share of total sales and consumer preferences leaning toward functional beverages that support immunity and stress relief. The recovery trajectory remains positive, underpinned by continued demand for health‑forward products.

Who are the major competitors in the North America Green Tea Market and what is the level of market consolidation?

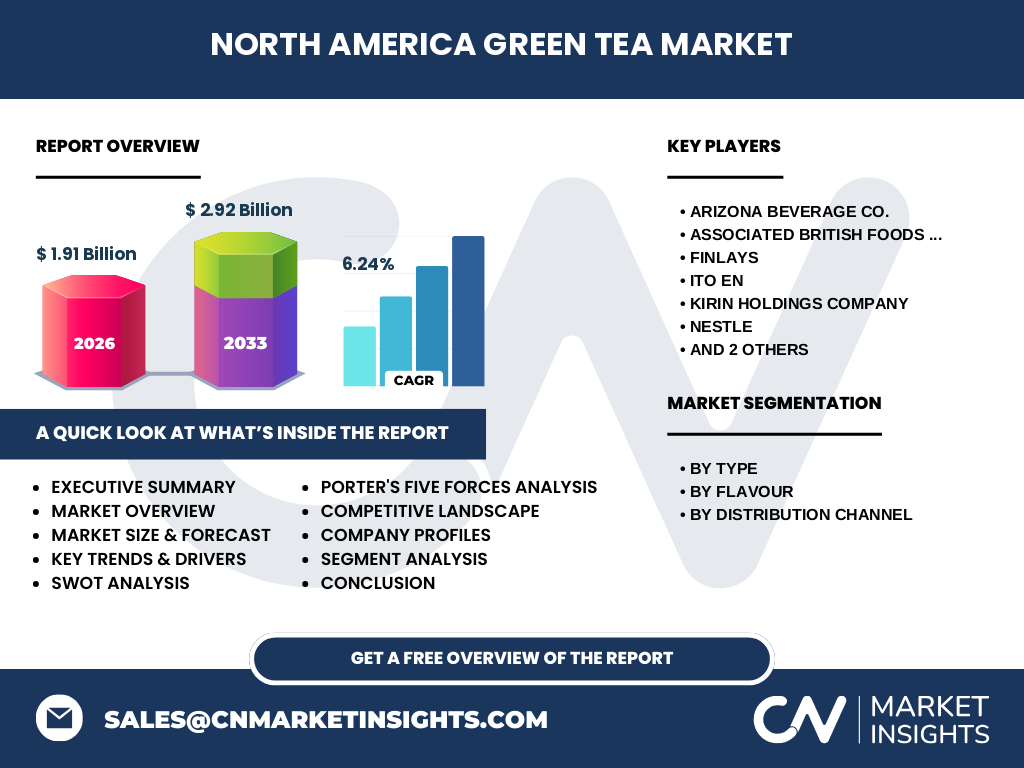

The market is moderately consolidated, led by multinational beverage and food companies. Key players include AriZona Beverage Co., Associated British Foods plc., Finlays, ITO EN, Kirin Holdings Company, Nestlé, Tata Global Beverages, and Unilever. These firms leverage extensive distribution networks, strong brand portfolios, and ongoing product innovation to maintain market leadership. While a few large firms dominate the mainstream segments, niche brands continue to carve out space in specialty and premium categories.

What are the high‑level findings in the Executive Summary?

The North America Green Tea Market is valued at $1.91 billion in 2026 and is projected to reach $2.92 billion by 2033, reflecting a CAGR of 6.24 % over the forecast horizon. Growth is fueled by health‑centric consumer trends, the expansion of flavored and ready‑to‑drink formats, and robust online sales channels. Leading companies are intensifying R&D to launch innovative flavors and sustainable packaging. While price sensitivity and supply‑chain constraints pose challenges, opportunities exist in functional blends, premium loose‑leaf offerings, and strategic partnerships that broaden distribution.

What are the North America Green Tea Market Forecasts for 2025‑2032?

Based on the provided CAGR of 6.24 %, the market is expected to maintain steady expansion throughout the 2025‑2032 period. Revenue growth will be driven primarily by the iced and flavored green tea categories, alongside a gradual increase in premium loose‑leaf sales. Online distribution is projected to capture an ever‑larger share, supported by consumer demand for convenient, home‑delivery options. Companies that invest in product diversification and sustainability are likely to outperform the market average.

How is the North America Green Tea Market sized and shared by segmentation?

Segmenting by type, green tea bags hold the largest portion due to their convenience and widespread availability, while instant mixes cater to quick‑brew consumers. Iced green tea is the fastest‑growing sub‑segment, driven by RTD trends, and loose‑leaf remains popular among connoisseurs. By flavour, lemon leads the market, followed by aloe vera and cinnamon, reflecting consumer appetite for tangy and exotic profiles. In terms of distribution channel, supermarkets and hypermarkets command the biggest share, with convenience stores providing niche reach and online channels showing the highest growth rate.

What is the global North America Green Tea Market size and share by region?

Within the global context, North America represents a significant consumer base for green tea, contributing a notable portion of worldwide sales. The region’s market size of $1.91 billion in 2026 underscores its importance, with the United States accounting for the majority of demand, followed by Canada and Mexico. The growth trajectory aligns with global trends toward healthier beverage choices.

What does the Regional Analysis of the North America Green Tea Market reveal?

The United States dominates the regional landscape, driven by large urban populations, advanced retail infrastructure, and strong health‑focused marketing. Canada shows steady growth, especially in specialty tea shops and online platforms. Mexico’s market remains smaller but is expanding as consumer awareness of green tea’s benefits increases. Regional differences are evident in flavor preferences, with lemon and vanilla being more popular in the U.S., while aloe vera gains traction in Canada’s wellness‑oriented segment.

What are the leading company profiles and their strategies in the North America Green Tea Market?

AriZona Beverage Co. focuses on RTD iced green tea, leveraging bold branding and value pricing. Associated British Foods plc. emphasizes premium loose‑leaf and organic certifications. Finlays capitalizes on supply‑chain expertise to deliver cost‑effective tea bags. ITO EN invests in functional blends with added vitamins. Kirin Holdings Company integrates green tea into its broader beverage portfolio, targeting convenience stores. Nestlé utilizes its global reach to promote flavored instant mixes. Tata Global Beverages pursues sustainable sourcing and innovative packaging. Unilever leverages its brand portfolio to expand distribution across supermarkets and online channels.

What does Porter’s Five Forces analysis indicate for the North America Green Tea Market?

Threat of new entrants is moderate; brand loyalty and economies of scale favor incumbents, but niche innovators can enter via online channels. Bargaining power of suppliers is moderate, as high‑quality tea leaf suppliers hold some leverage, yet large players can negotiate favorable terms. Bargaining power of buyers is high, given price sensitivity and abundant alternatives. Threat of substitutes is significant, with coffee, black tea, and other functional drinks competing for the same health‑conscious segment. Industry rivalry is intense, driven by product innovation, flavor diversification, and aggressive marketing.

What are the SWOT insights for the North America Green Tea Market?

Strengths: Strong health perception, diverse product formats, and growing demand for natural beverages. Weaknesses: Higher price points relative to some alternatives and reliance on imported raw material. Opportunities: Expansion of flavored and functional variants, sustainable packaging, and digital commerce. Threats: Competitive pressure from coffee and other functional drinks, regulatory scrutiny on health claims, and potential supply disruptions.

How does the value chain of the North America Green Tea Market function?

The value chain begins with cultivation of Camellia sinensis leaves, primarily sourced from Asia. These leaves undergo processing (steaming, drying, grinding) before being packaged as bags, instant mixes, or bulk loose leaf. Flavoring agents are added during formulation for flavored variants. Distribution channels—supermarkets, convenience stores, and online retailers—then deliver the finished product to end consumers. Value‑adding activities include branding, marketing, and sustainability initiatives that differentiate products in a crowded marketplace.

What key investment insights can be drawn for the North America Green Tea Market?

Investors should target companies that demonstrate strong innovation pipelines, especially in RTD iced teas and functional flavored blends. Brands with robust e‑commerce capabilities and sustainable packaging are positioned for premium pricing and loyalty. Strategic acquisitions of niche specialty tea producers can provide entry into the premium loose‑leaf segment. Partnerships with health‑focused influencers and wellness platforms can amplify brand reach and justify higher margins.

What are the concluding takeaways for the North America Green Tea Market?

The market is on a clear growth path, underpinned by a 6.24 % CAGR and a projected reach of $2.92 billion by 2033. Health trends, flavor innovation, and digital distribution are the primary catalysts. While price competition and supply challenges persist, companies that invest in product differentiation, sustainability, and omnichannel strategies are likely to capture the most value.

What research methodology was employed for this report?

The study combined primary interviews with industry executives, retail buyers, and consumer focus groups, alongside secondary data from company filings, market databases, and trade publications. Trend analysis, competitive benchmarking, and financial modeling were used to validate the forecast and derive market sizing.

What is the scope of this research?

The research covers the North American region, encompassing the United States, Canada, and Mexico. It addresses product types, flavors, and distribution channels, and focuses on the period from 2025 to 2032. The scope excludes detailed country‑by‑country revenue breakdowns beyond the provided aggregate figures.

Which key companies and recent developments are highlighted in the North America Green Tea Market?

Key players include AriZona Beverage Co., Associated British Foods plc., Finlays, ITO EN, Kirin Holdings Company, Nestlé, Tata Global Beverages, and Unilever. Recent developments feature AriZona’s launch of a low‑calorie iced green tea line, Nestlé’s introduction of organic instant mix packs, ITO EN’s partnership with a North American wellness brand to create vitamin‑fortified blends, and Unilever’s rollout of recyclable packaging across its green tea portfolio.